Published

I Got $4.84 From a Class Action Settlement and They Really, Really Didn't Want Me to Have It

So here's the thing. When a company loses a class action lawsuit and has to pay millions to regular people, they don't just write you a check. They go out of their way to make sure you never actually get to spend your cut. I'm not being dramatic. I have receipts.

Over the past couple years I've gotten several emails. "You're eligible for a settlement payment."

I click the link. What do I get? Not a check. Not a direct deposit. Not anything normal. I get a virtual debit card. Add it to Apple Wallet. Done.

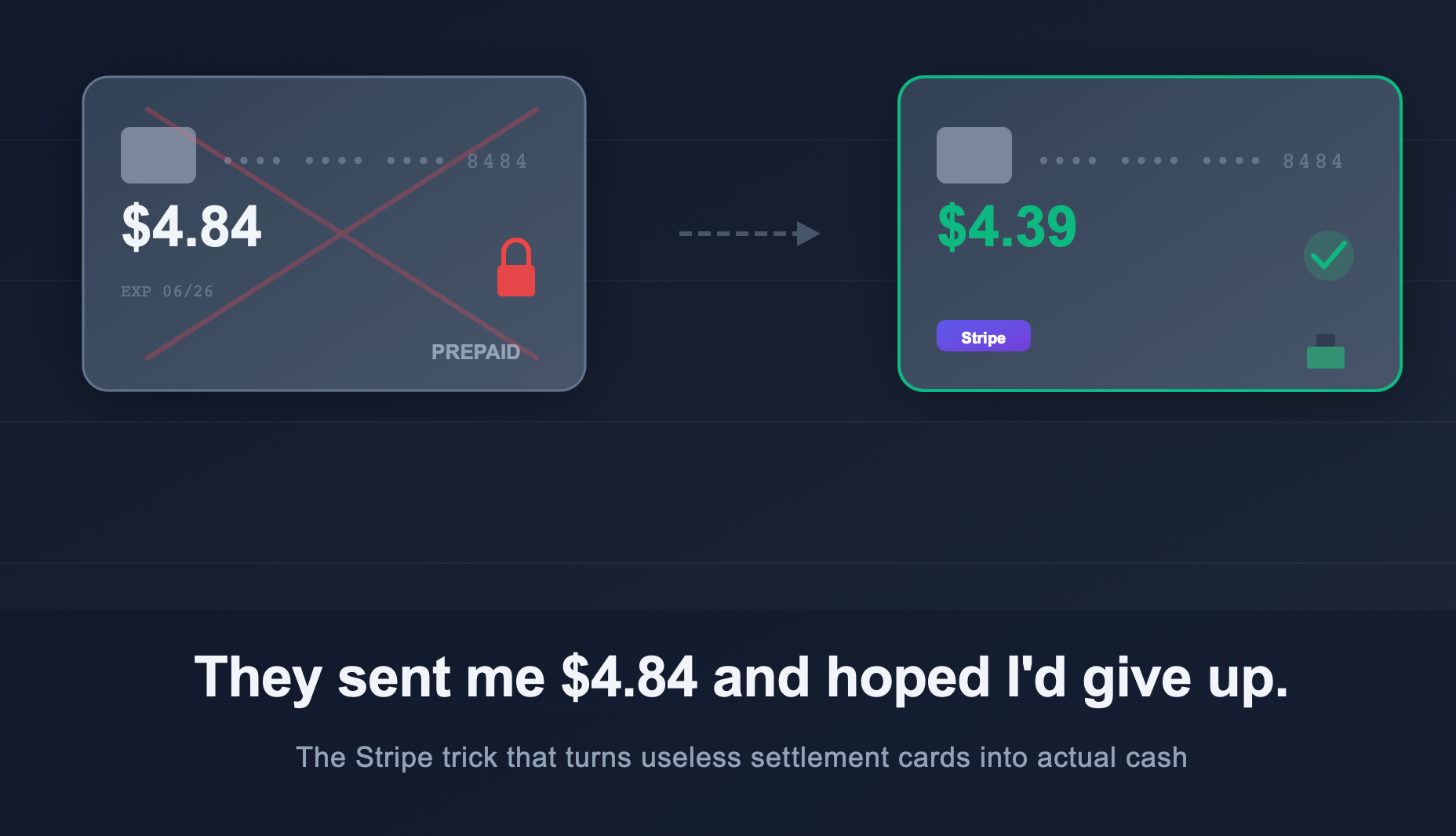

One of them was for $4.84.

Four dollars. And eighty-four cents.

Now look — I'm not out here complaining about free money. But nobody sends you $4.84 on a restricted debit card because they're hoping you'll enjoy it. They send it that way because they're betting you'll give up before you figure out how to spend it.

I've collected a bunch of these. Class action settlements. Data breach payouts. Random consumer protection stuff I forgot I even signed up for. Every single one works the same way. Email. Link. Virtual card. Some weird amount like $11.37 or $27.62.

The balances added up. So did the restrictions.

No ATM. No cash back at a register. Can't use it at a gas station. Can't add it to Venmo. Can't add it to PayPal. Can't transfer it to your bank. Oh, and it expires. If you don't spend every cent before the expiration date, the card company keeps whatever's left.

Thanks for playing.

I got curious and started searching around. Turns out I'm not the only one. There's a whole community of people online who can't get their settlement money off these cards. Three of my cards came from myprepaidcenter.com so I looked them up first — pages and pages of complaints. Cards that randomly decline. Balances that shrink from "inactivity fees." Customer service that puts you in a phone tree maze designed to exhaust you into hanging up.

And look, it's not just them. myprepaidcenter just happens to be the one I got stuck with three times. Every company in this business runs the same game. The pattern isn't subtle.

Wait, Isn't This Kind of Illegal?

Funny you should ask.

In California, if you have a gift card with less than $10 on it, you can walk into the store and ask for cash. It's the law. They have to give it to you. Gift cards in California also don't expire. Also the law.

But settlement debit cards? Those don't count. They're not "gift cards" in the legal sense. Even though that's exactly what they are — your money, sitting on a card, that you're supposed to spend.

Same person. Can walk into Starbucks with a $4.84 gift card and demand cash. That's protected. Has a $4.84 settlement debit card? Zero rights. Same amount. Same basic thing. Completely different rules.

That gap isn't an accident. Someone made sure it was there.

I Asked AI For Help. Bad Idea.

So I did what anyone does in 2026. I asked AI how to get my money off these cards.

The suggestions were all terrible.

ATM? Blocked. Every card says no ATM access right in the fine print.

Buy gas? Declined. The pre-authorization at the pump won't approve a $4.84 card.

Venmo? PayPal? These cards are hard-coded to reject peer-to-peer platforms.

Money order? Blocked.

Buy an Amazon gift card for the exact amount? Okay, I'll give AI this one — but now what? I've got a $4.84 Amazon credit instead of a $4.84 prepaid card. Same problem, different logo. Also, try spending exactly $4.84 on Amazon with zero leftover. You can't do it. Tax. Minimums. Weird totals. You leave 34 cents behind every time.

Multiply that 34 cents by a few million people and suddenly the entire business model makes sense.

The restrictions aren't bugs. They're the whole point. Every abandoned balance, every expired card, every 63 cents someone couldn't spend — that's revenue. Pure profit.

I almost gave up.

And Then I Remembered Stripe

I run a business. I get paid through Stripe.

Stripe has this thing in the dashboard. "Create a payment." Manual charge. You type a name, a card number, an amount. Click a button. Done.

No code. No setup. Just a form.

So I went into my Stripe dashboard. Put my own name as the customer. Punched in the card number and details from the virtual settlement card. Entered the exact balance left on it. Hit submit.

It went straight through.

Two days later the money landed in my bank account. Minus Stripe's cut — 2.9% plus 30 cents.

Here's the math on that $4.84 card:

| What I tried | What I got |

|---|---|

| Try to spend it somewhere | Maybe most of it. Maybe none. |

| Let it expire | $0.00 |

| Stripe it to myself | $4.39 cash in my bank |

I'll take $4.39 over zero every time.

And that $4.84 card is the worst case. The tiny one. For the bigger settlements it's even better. I had a $200 card — Stripe took about six bucks and 194 landed in my account. Actual money. In my actual bank. That I can actually spend.

I've done this a dozen times now. Every single card worked.

Why? Because these prepaid cards don't block everything. They block specific merchant category codes — the ones for ATMs and money transfers and anything that smells like cash. Stripe codes as a regular online purchase. The card network sees "e-commerce transaction" and approves it. That's the whole trick.

Now, if this were just a life hack about debit cards, I'd stop here. But it's not really about the debit cards. It's about how I operate. Show me a system designed to wear people down until they quit, and my first instinct isn't to complain — it's to find the crack. The $4.84 card? That's just the most recent example. I've been doing this my whole life. Fine print, loopholes, workarounds. I don't get tired. I don't get bored. I don't give up.

Here's the Actual Point

If you're sitting on settlement debit cards with stupid balances, the instructions are simple. Open a Stripe account (free). Go to your dashboard. Create a manual payment. Enter the card details. Cash yourself out. You lose about 3%. That's it.

97% of something beats zero every time. I've done it a dozen times. It works.

But here's why I really wrote this.

Some people look at a locked door and go find another door. I look at the lock. I figure out how it works. Then I walk through.

That's not a metaphor. It's just how I'm wired. Gift card has $4.84 and the rules say I can't cash it? Fine. I'll find a way. Company sends me a 30-page terms of service and bets I won't read it? Wrong bet. Someone structures a settlement so the money technically belongs to me but I can't actually access it? I'll spend a Saturday figuring out the bypass.

I'm not trying to sound tough. I'm just telling you what happens when you put an obstacle between me and something I'm owed.

The card companies that built their business on breakage — on people giving up, letting balances expire, walking away from money that's rightfully theirs — they counted on most people not being like me. And honestly? That math probably works for them most of the time.

But if you're dealing with me specifically? Different equation.

I keep records. I read the fine print. I find the workaround. I don't get bored. I don't get tired. And when I figure something out, I don't keep it to myself.

So if you're in the business of hoping people give up and go away — you should hope I'm not on the other end of it.

This is my personal experience. Not legal advice, not financial advice, not an endorsement of Stripe or anyone else. If you're in active litigation, ask your lawyer before posting about it.